The Corporate Sustainability Reporting Directive (CSRD)

In January 2023, the EU’s Corporate Sustainability Reporting Directive (CRSD) came into effect, making it mandatory for around 50,000 companies to adhere to a whole new set of sustainability reporting requirements.

This includes companies spanning all kinds of industries and sizes, and over 10,000 non-EU companies that operate within the EU.

The first set of companies affected need to begin compiling data in 2024, with the first report due in 2025. And the rest of the deadlines aren’t far behind, so businesses need to start getting prepared to comply sooner rather than later.

If you want to find out more about the CSRD, we’re here to help. We’ve put together this guide for you to find out everything you need to know, from timelines and requirements, to reporting and compliance.

Contents

The Corporate Sustainability Reporting Directive (CSRD)

- What is the CSRD?

- What are some of the key CSRD requirements?

- Who needs to comply with the CSRD and when?

- What happens if you don’t comply with the CSRD?

The European Sustainability Reporting Standards (ESRS)

- What are the ESRS?

- What are the general requirements standards?

- What are the environmental standards?

- What are the social standards?

- What is the governance standard?

- What is the double materiality requirement?

Getting started with reporting

What next?

What is the CSRD?

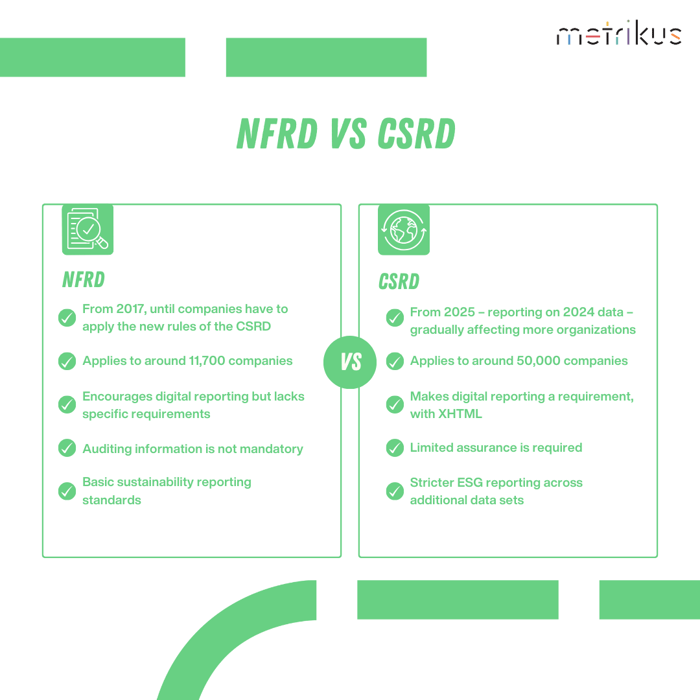

The Corporate Sustainability Reporting Directive (CSRD) is basically an upgraded replacement of the EU’s Non-Financial Reporting Directive (NFRD).

It has stricter reporting standards – the European Sustainability Reporting Standards (ESRS) – and covers an additional 40,000 companies. It also complements two other regulations which go in the same direction: the Sustainable Finance Disclosure Regulation (SFDR) and the EU Taxonomy.

The main purpose of the CSRD is to ensure consistent and comparable reporting of environmental, social, and governance (ESG) performance. In comparison to the NFRD, it has a bigger focus on the S and G of ESG, as well as stricter requirements around digital reporting and auditing to boost credibility and accuracy.

What are some of the key CSRD requirements?

We’ll dig a bit deeper into the actual reporting standards later on, but for now, there are some key requirements you should know about.

- Yearly check-ins

Each year, companies will have to publicly report on their ESG performance aligned to the ESRS.

- Reporting scope

It’s not just about your own operations – the CSRD requires you to report on your entire value chain.

- Mandatory due diligence

You need to get prepared to be open about your due diligence processes and results.

- Double materiality assessment

You’ll have to do a double materiality assessment to determine which requirements are relevant for your company.

- Auditing

You’ll need to get limited assurance for your reporting from a third party.

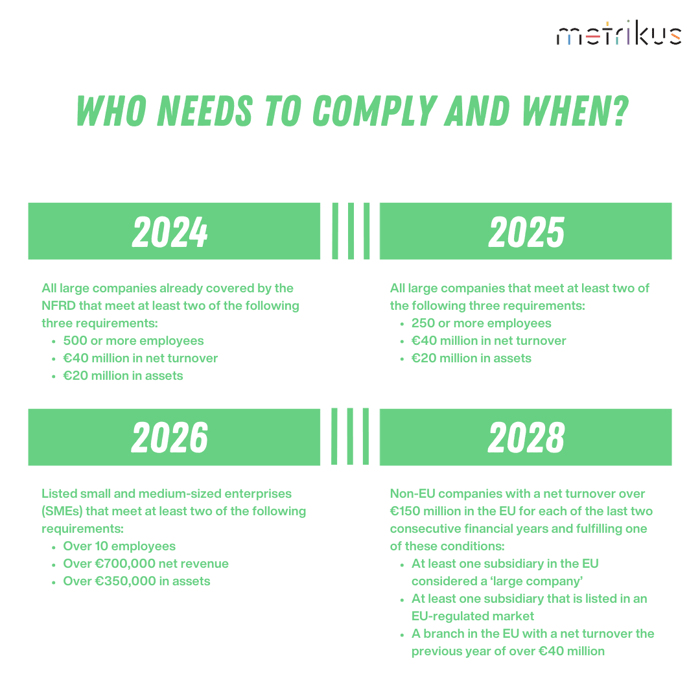

Who needs to comply with the CSRD and when?

The CSRD officially entered into force in 2023, but the reporting requirements are going to be rolled out in phases for different types of companies over the next couple of years.

Just to note, these dates and figures are correct as of October 2023, but the Commission keeps making changes. We will keep this updated as and when we hear more information!

2024

All large companies already covered by the NFRD that meet at least two of the following three requirements:

- 500 or more employees

- €40 million in net turnover

- €20 million in assets

2025

All large companies that meet at least two of the following three requirements:

- 250 or more employees

- €40 million in net turnover

- €20 million in assets

2026

Listed small and medium-sized enterprises (SMEs) that meet at least two of the following requirements:

- Over 10 employees

- Over €700,000 net revenue

- Over €350,000 in assets

2028

Non-EU companies with a net turnover over €150 million in the EU for each of the last two consecutive financial years and fulfilling one of these conditions:

- At least one subsidiary in the EU considered a ‘large company’

- At least one subsidiary that is listed in an EU-regulated market

- A branch in the EU with a net turnover the previous year of over €40 million

What happens if you don’t comply with the CSRD?

It’s up to each member country to decide what sorts of penalties should be imposed on companies that don’t comply with the CSRD. However, the EU has already put forward a set of recommended sanctions, including:

- A public declaration describing the company’s wrongdoing

- A cease-and-desist order against the guilty company

- Heavy fines for the offending company

It’s also thought the penalties could be similar to those under the NFRD. These consist of fines of €25,000 or imprisonment for individual directors, and fines of either €10 million or 5% of the company’s global annual turnover – whichever is highest.

There are also lots of other reasons for your company to start compiling with the CSRD:

- Future-proofing your company against upcoming regulations

- Reducing your company’s impact on the environment

- Making your company a better place for employees to work

Now we’ve covered the basics of the CSRD, it’s time to give you the lowdown on the reporting standards themselves – the ESRS.

The European Sustainability Reporting Standards (ESRS)

The European Sustainability Reporting Standards (ESRS) are the set of standards that companies subjected to the CSRD will need to comply with.

The goal is make it easier to compare ESG performance between companies, which is currently one of the big issues when it comes to reporting.

Keep reading to find out what the standards cover, and how the mandatory double materiality assessment is going to work.

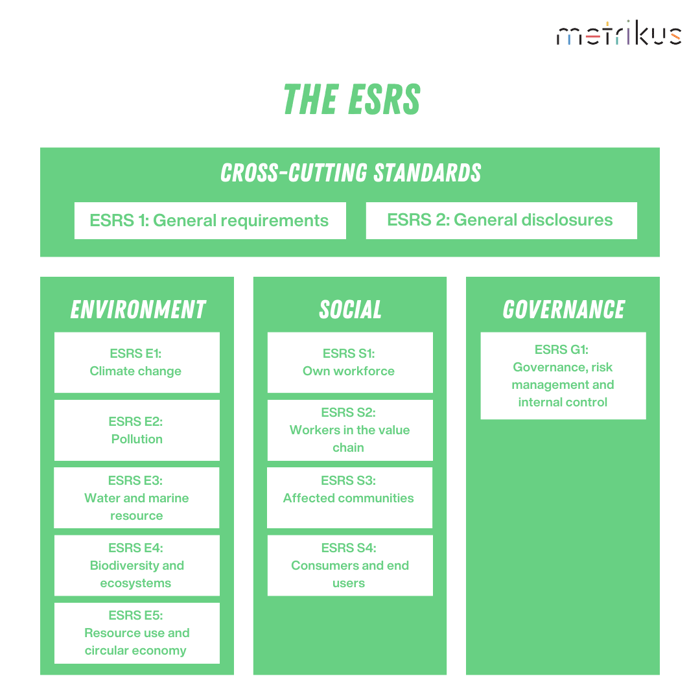

What are the ESRS?

The 12 ESRS set out specific requirements that companies need to align with when reporting their sustainability practices. They are sector-agnostic, meaning that all companies can complete the sections regardless of industry.

There are two cross-cutting standards, and 10 topical standards covering environmental, social and governance aspects.

It’s expected that under the 12 ESRS, there will be a massive 85 indicators and 1,100 data points, which will be measured both quantitatively and qualitatively.

What are the general requirements standards?

You can think of the general requirements standards as the base of your reporting, as they tell you what information you need to include and how you need to present it.

- ESRS 1: General requirements

- ESRS 2: General disclosures

The general disclosure standard is the only one that everyone must follow. To figure out the other disclosures that apply to you, you’ll need to do a double materiality assessment which we’ll explain in a little bit.

What are the environmental standards?

The environmental standards (ESRS E1 to E5) are all about how to report your company’s impact on the environment.

Currently, there are a total of five standards that cover the following areas:

- ESRS E1: Climate change

- ESRS E2: Pollution

- ESRS E3: Water and marine resources

- ESRS E4: Biodiversity and ecosystems

- ESRS E5: Resource use and circular economy

Companies with fewer than 750 employees will have the option to exclude certain disclosure requirements. During their first year, they can omit reporting on their scope 3 emissions, and they don't need to report on biodiversity for the first two years.

What are the social standards?

The four social standards (ESRS S1-S4) cover – you guessed it – things that affect people, including:

- ESRS S1: Own workforce

- ESRS S2: Workers in the value chain

- ESRS S3: Affected communities

- ESRS S4: Consumers and end users

Again, companies with fewer than 750 employees will be able to exclude certain disclosure requirements.

During their first year of implementing the standards, they don’t need to report on their own workforce, and for the first two years, they can exclude information on workers in the value chain, affected communities, and consumers and end users.

What is the governance standard?

The governance standard (ESRS G1) outlines what companies need to report on in terms of their company’s conduct.

- ESRS G1: Governance, risk management and internal control

In the updated draft, the commission made some changes to requirements about corruption and bribery, as well as the protection of whistleblowers, to avoid any conflict with protection against self-incrimination.

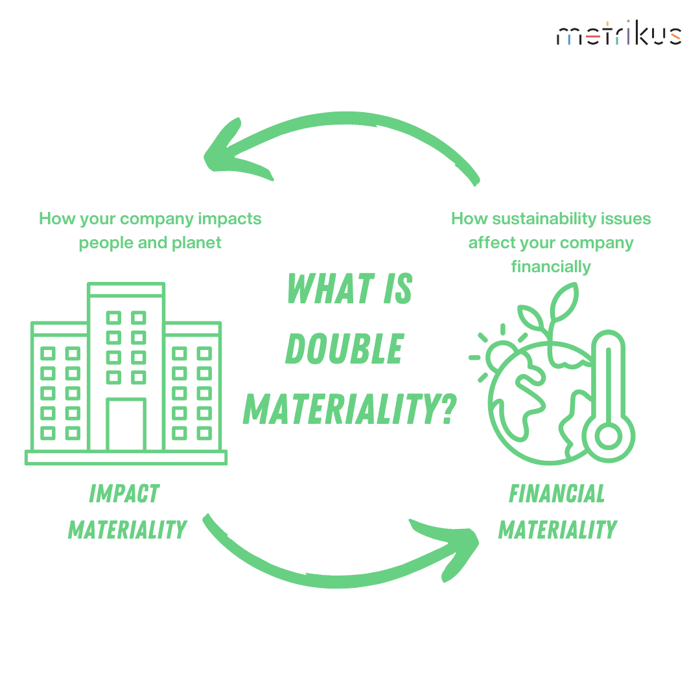

What is the double materiality requirement?

When it comes to reporting under the ESRS, the first step is for companies to carry out a double materiality assessment.

‘What on earth is that?’, we hear you ask. In essence, double materiality requires that companies report not only on how their business is impacted by the climate, but also how their activities impact the environment around them.

It is all about looking at financial materiality and impact materiality holistically. And the aim of the assessment is to determine which ESRS requirements are relevant for your specific organization.

1. Impact materiality

Impact materiality is all about how your company’s actions affect people and the planet in the short, medium, and long term. And remember, it’s not just about your own operation, you also need to assess the impact across your entire value chain.

2. Financial materiality

Here, the focus shifts to how sustainability issues impact your business financially. This includes factors like your company’s growth, performance, and cost of capital, in the short, medium, and long term.

By combining these two factors, you can figure out which risks and opportunities are material and should be included in your reporting.

It’s important to use appropriate thresholds to help you make this decision, including the likelihood of occurrence and the potential financial effect. This way, you can make sure you include the most important information in your CSRD report.

Getting started with reporting

How can companies get started with reporting?

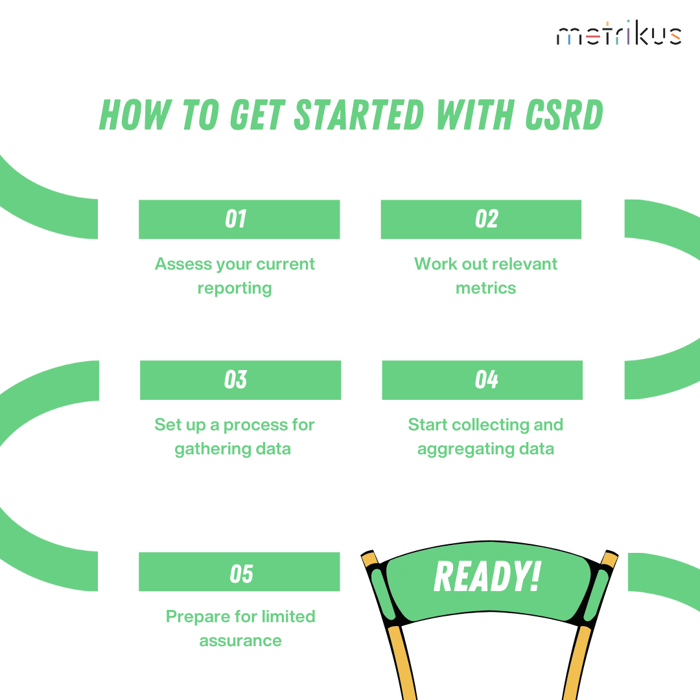

Getting started with your CSRD reporting might feel like a daunting task, but there are some steps you can take to get ahead of the game now.

- Assess your current reporting

Start by reviewing the sustainability framework your company currently follows and figure out how much work needs to be done for you to align with the CSRD.

You’ll probably find that there are lots of existing processes that you can continue using to incorporate the CSRD framework into your business.

- Work out which metrics are relevant to your company

Carry out a double materiality assessment to identify relevant ESRS impacts, risks and opportunities.

Even if some of the ESRS aren’t relevant to your company right now, it might be worth looking ahead to consider which requirements you’ll need to start reporting on in the near future.

- Set up a process for gathering data

To comply with the CSRD, you need to gather a lot of data from your suppliers, operators, and partners. And as we all know, getting external companies to share their data isn’t always an easy task.

This means it’s really important to set up a clear and straightforward process for sharing, collecting, and organizing the data that works for all the stakeholders involved.

- Start collecting and aggregating data

As we always say, you can’t manage what you don’t measure. Our advice for any company out there is to start collecting as much relevant data as you can.

Calculating your scope 3 emissions – indirect emissions caused by your value chain – tends to be a long and tricky task, so it’s a good idea to get started on this sooner rather than later.

And remember, important data will need to be digitally tagged, so make sure you’re collecting your information in the right format from the outset.

- Prepare for limited assurance

As we’ve mentioned already, the CSRD introduces a more robust approach toward the assurance of sustainability information.

You’ll need to obtain limited assurance, and include an assurance report along with your sustainability report. Like collecting data, this can be a lengthy process so we’d advise you start preparing for auditing now.

What about other reporting standards?

You might be worried about doubling up on reporting, but luckily for you, a big focus of the CSRD is the interoperability of reporting.

The ESRS incorporate existing EU legislations and frameworks like the Task Force on Climate-Related Financial Disclosures (TCFD), Sustainable Finance Disclosure Regulation (SFDR) and the EU Taxonomy. And there’s also a very high level of alignment between the ESRS, the standards of the International Sustainability Standards Board (ISSB) and the Global Reporting Initiative (GRI).

All these acronyms might be hard to remember, but there’s no need to feel overwhelmed. The point we’re making is that regulatory bodies are working to align so that you can collect data once and repurpose it across multiple disclosures.

What next?

What’s coming next with the CRSD and ESRS?

Member states have until 6th July 2024 to transpose the CSRD into their national laws and bring into force regulations and administrative provisions necessary for compliance.

There are also going to be some more standards published, including sector-specific standards for:

- Oil and gas

- Coal

- Quarries and mining

- Road transport

- Agriculture

- Farming and fisheries

- Motor vehicles

- Energy production and utilities

- Food and beverages

- Textiles, accessories, footwear, and jewelry

And additional standards tailored to:

- Listed SMEs

- Non-listed SMEs

- Non-EU entities

We still haven’t been told much about the content of these additional standards, but the European Financial Reporting Advisory Group (EFRAG) has stated they will be ‘proportionate and relevant to the scale and complexity of the activities, and to the capacities and characteristics of the entities for which they are designed.’

It’s safe to say that this leaves a lot of questions left unanswered, but this doesn’t mean you should ignore the upcoming legislation.

Whatever the size, industry, or location of your company, it’s worth laying the groundwork for CSRD now to make sure your company is ready to comply when the time comes.

Get in touch

If you have any feedback or questions about this guide or CSRD in general, we’d love to hear from you. The best person to contact is Sami Mustapha, our ESG & Sustainability Lead – his email is sami@metrikus.io.

And if you want to stay up to date with the latest Metrikus content, make sure you sign up to our newsletter.